what evidence is necessary to demonstrate the ability to defer settlement of short-term debt

June 21, 2021

Primary markets for brusque-term debt and the stabilizing effects of the PDCF

Mark Carlson and Marco Macchiavelli

Introduction

During early on March 2020, amid rapidly spreading restrictions associated with preventing the spread of COVID-19, financial markets came under immense strain. These strains ultimately spilled over to funding markets and to institutions that are highly dependent on such markets. Included amid those afflicted financial institutions were the primary dealers, who are key intermediaries in many financial markets. The Federal Reserve took deportment to support the liquidity of the primary dealers through the establishment of the Master Dealer Credit Facility (PDCF). The PDCF provided the primary dealers with a stable funding backstop and was intended to enhance the ability of the dealer to, in turn, back up smooth market functioning and facilitate the availability of credit to businesses and households. In this Note, we examine whether the PDCF enhanced the power of the dealers to provide intermediation services in ways that benefitted their customers. Nosotros find evidence that this was indeed the case.

The particular intermediation service provided by the primary dealers that we investigate in this Note is their office in facilitating the issuance of commercial newspaper (CP) and negotiable certificates of deposit (CDs). Commercial paper is a short-term debt security issued by both financial and non-financial companies to raise money that directly supports a wide range of economical activity—similar coming together the issuers' solar day-to-day operational needs such as payments for inventories and payrolls. Negotiable certificates of deposit are issued by banks in large denominations, well above the deposit insurance limit, to enhance dollar funding in wholesale funding markets.1 Many CP and CDs issuers depend on dealers to help in the issuance process.2 Dealers provide this back up by purchasing the paper from the issuers and and so re-selling it to other investors, such every bit money market mutual funds, other mutual funds, and corporations with excess greenbacks. In fulfilling this intermediation role, dealers incur funding hazard. To the extent that dealers were experiencing funding challenges during the early days of the pandemic, they might accept charged CP and CD issuers more to assist with the issuance process or only been able to aid with issuance of smaller amounts.

Nosotros are interested in testing whether the funding backstop provided to the chief dealers past the PDCF benefited the dealers' customers, specifically corporations that rely on dealers for issuing CP and CDs. Our results show that the ability of dealers to pledge CP and CDs to the PDCF did benefit the issuers of those securities. Specifically, these issuers were able to consequence in greater size or at lower toll when the CP or CD that was issued was pledged as collateral to the PDCF by the dealer.

It is unremarkably understood that merely providing the selection to pledge collateral at the PDCF, whether exercised or not, should contribute significantly to stabilizing short-term funding markets by providing a source of funding backstop to the dealers that intermediate these markets. In this Note we go 1 step further and show that the bodily pledge of a specific security to the PDCF provided boosted benefits to the issuer of such security. This result suggests that, during a stress event, dealers may be more challenged in providing intermediation services amongst heightened funding risks. Every bit a outcome, beingness able to pledge a newly issued security may exist particularly benign in alleviating those funding risks while the dealer is in the process of placing the security to the ultimate investors.

Background on the PDCF and its utilise past the primary dealers

The PDCF supported dealer funding liquidity past offering loans to the dealers at a rate of 25 basis points, which implies a spread to reference rates higher than typically paid by dealers in ordinary times just considerably below the rates bachelor in the market during periods of stress. Loans from the PDCF had a maturity of upward to 90 days but could be pre-paid at any time by the dealer. All PDCF loans were collateralized, with a broad range of securities eligible to serve as collateral. Importantly for our analysis, dealers were able to pledge investment grade CP and CDs as collateral when receiving a loan through the PDCF. By allowing dealers to borrow against such collateral, that should have helped convalesce funding pressures at the dealers themselves.

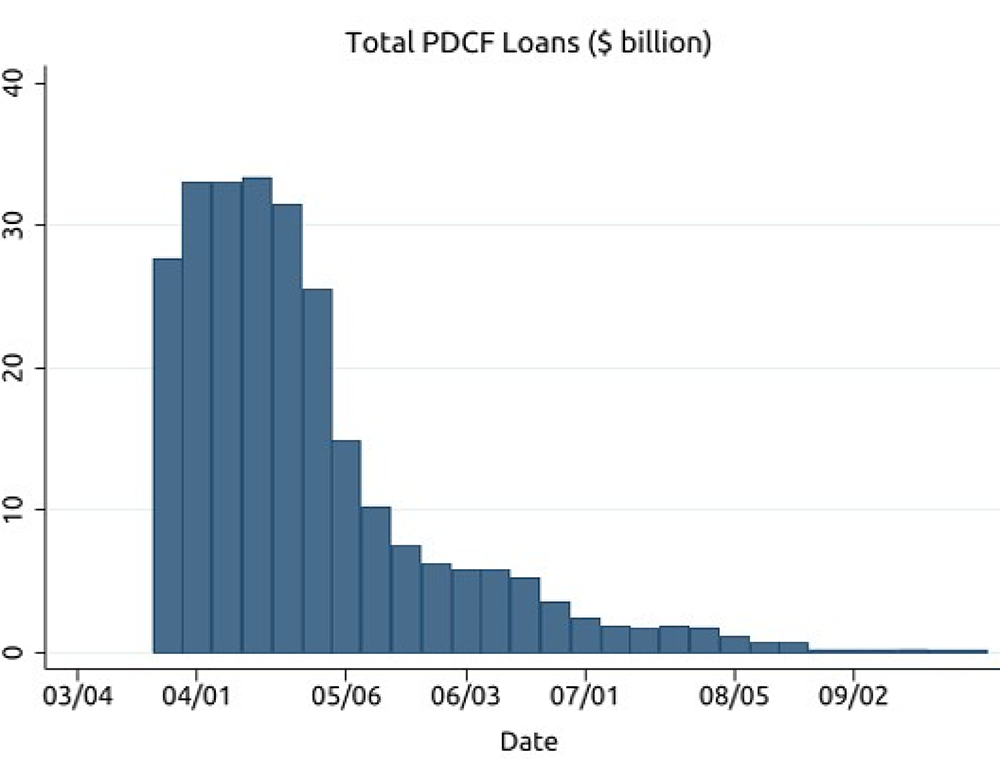

Use of the PDCF by the primary dealers was heaviest in late March 2020. Within a few days of the facility being opened on March twenty, the primary dealers had borrowed over $xxx billion from the facility. Utilize stayed fairly steady for a few weeks and so began to decline effectually the terminate of April. By mid-May dealer borrowing from the PDCF had dropped quite essentially as funding markets normalized. (Come across Figure 1 which reports total PDCF loans outstanding each calendar week from March 2020 to December 2020.)

Figure i. Total PDCF Loans Outstanding ($ billion)

Dealers were able to pledge a wide range of collateral to the PDCF, all subject to appropriate haircuts. We estimate that, by value, roughly 20 percent of collateral pledged during the period nosotros study consisted of CP or CDs.3

Touch on on CP and CD issuers

Nosotros are interested in whether at that place were any benefits to issuers of CP and CDs from dealer use of the PDCF. Equally noted above, we certainly look that this is true in a general sense. The existence of the PDCF as a funding market backstop generally improved conditions in coin markets, including for CP and CD issuers. Nevertheless, during a stress outcome, dealers may face up more liquidity risks and challenges in providing intermediation services. In this case, the ability of dealers to pledge CP and CDs to the PDCF may accept been particularly beneficial to the issuers of those instruments. To examine this, we test whether pledges of particular pieces of collateral, as indicated by the CUSIP, are associated with college issuance volumes or lower chief market spreads on that CUSIP.4

We bear our analysis using ii datasets. Security-level data on primary marketplace issuance of CP and CDs is obtained from DTCC Solutions LLC, an affiliate of The Depository Trust & Clearing Corporation (DTCC).5 The data include CUSIP, issuer name, issuance and maturity dates, amount issued, and yield. We compute the primary market place spread of each security by taking the difference between its yield at issuance and the overnight indexed swap (OIS) rate at equivalent tenor. A further slice of data available in this data that we utilise later is whether the CP or CD was placed to investors directly past the issuer or through a dealer who purchases the issuance and and so sells information technology to investors. The CP information too include the credit ratings associated with the issue, with most of the issuance in the top two notches, A1/P1 and A2/P2.six

Nosotros also apply data on usage of the PDCF.7 In particular, we use information on the identity of the dealer borrowing/pledging particular pieces of collateral, the CUSIP of the pledged securities, the value of the collateral pledged, the amount of the loan to the dealer, the date the loan is extended, and the interest rate. The PDCF was announced on March 17 and became operational on March xx.

These two data sets are merged so that we have information on the amounts and pricing of item CP and CDs when they are issued and nosotros also know whether they were pledged at the PDCF. Our sample spans the period from March 1, 2020, at the eve of the crisis, to Apr 30, 2020 when, every bit noted above, use of the PDCF had diminished notably. Data prior to the implementation of the PDCF (March 1 to March xix), while not used to estimate the outcome of the PDCF, are nevertheless useful for estimating stock-still furnishings and standard errors more precisely.

In our assay, we first regress issuance volumes on an indicator for whether or not CP or CDs from that issuer were pledged equally collateral to the PDCF. Specifically, we gauge the following panel regression:

$$$ Log(Issuance)_{ct} = \beta \cdot {Pledged}_{ct} + \mu_t + \mu_i + \varepsilon_{ct} $$$

Where $$Log(Issuance)_{ct}$$ is the logarithm of one plus $${Issuance}_{ct}$$ in $ 1000000. $${Issuance}_{ct}$$ equals zero if CUSIP $$c$$ has no issuance on 24-hour interval $$t$$ or the amount of CUSIP $$c$$ issued if strictly positive. Therefore, the panel contains days in which a CUSIP is issued $$(Log(Issuance)_{ct} > 0)$$ and days in which it is not $$(Log(Issuance)_{ct} = 0$$. This way nosotros can capture instances in which a CUSIP is issued and pledged too equally instances in which at that place is no issuance but the CUSIP is nevertheless pledged, possibly to finance secondary market transactions. The contained variable of interest, $${Pledged}_{ct}$$, equals one if CUSIP $$c$$ is pledged as collateral at the PDCF for a new loan on day $$t$$. Since we are interested in whether the PDCF supports primary market place issuance, we prepare $${Pledged}_{ct}$$ to equal one simply if a new PDCF loan is originated on day $$t$$ with CUSIP $$c$$ pledged equally collateral. During the subsequent days in the life of the PDCF loan that has CUSIP $$c$$ pledged as collateral, $${Pledged}_{ct}$$ is set to zero. We expect separately at the highest quality of CP (rated A1/P1), slightly lower quality CP (rated A2/P2), and CDs. Solar day fixed effects ($$\mu_t$$) are included in all specifications and issuer fixed effects ($$\mu_i$$) are included in some specifications. Notice that each issuer $$i$$ tin result multiple CUSIPs, each one with different maturity. Standard errors are double-clustered at the issuer and 24-hour interval levels.

Table ane. Primary Market Issuance and PDCF Usage

| (ane) | (2) | (three) | (4) | (5) | (vi) | |

|---|---|---|---|---|---|---|

| Pledged | 0.585*** | 0.306*** | 0.765*** | 0.524*** | 0.086 | 0.056 |

| (0.166) | (0.104) | (0.251) | (0.188) | (0.102) | (0.097) | |

| Sample | A1P1 CP | A1P1 CP | A2P2 CP | A2P2 CP | CD | CD |

| Obs. | 319,742 | 319,738 | 92,544 | 92,540 | 639,324 | 639,324 |

| R-squared | 0.002 | 0.269 | 0.006 | 0.261 | 0.001 | 0.021 |

| Day Fe | ✔ | ✔ | ✔ | ✔ | ✔ | ✔ |

| Issuer FE | ✔ | ✔ | ✔ |

Under the hypothesis that the PDCF supports chief marketplace issuance, we should detect that pledging a CUSIP at the PDCF is associated with a greater amount issued. The results of this analysis are in Table 1. Nosotros indeed find that at that place is a positive association between the amount of CP that an issuer issued during the stress period and having that security pledged by a dealer to the PDCF. For instance, every bit indicated in column (2), a new pledge of A1/P1 commercial paper is associated with an increase in Log(Issuance) past 0.3, which represents a boost in issuance of about 10% of the boilerplate Log(Issuance). This association is even stronger for A2/P2 paper. We practice non find a similar association for CDs.

These results overall suggest that the PDCF supported primary marketplace issuance. Fifty-fifty if our simple regression cannot demonstrate a strict causal human relationship between pledging CP and issuance, the positive association between issuance and PDCF pledge indicates that dealers used PDCF loans to finance the buy of larger CP issuances. This is consistent with the PDCF providing support to CP issuance by offering backstop financing to the dealers. Indeed, under normal circumstances, in that location would exist no demand for dealers to use the PDCF even for larger CP issuances.

Next, nosotros look at the pricing of CP and CDs and whether or not securities that were pledged at the PDCF as collateral were priced differently than other like securities. To do and so, we bear similar regressions to issuance, merely this time using the spread on each CUSIP as our dependent variable and whether or not that CUSIP was pledged to the PDCF as our independent variable. The spread (in percentage) is computed every bit the yield at issuance minus the OIS rate at comparable tenor. In this sample, we only go on issuance days so that we only have observations with non-missing spreads. We find, every bit shown in Table 2, that the primary market spread was lower for CDs that were pledge to the PDCF as collateral than for other CDs.8 Indeed, the master market spread on CDs that were pledged was 30 basis points (or 0.3 percent) lower than like CDs. The issue is non only statistically but likewise economically meaning, every bit the average spread for CDs is 130 basis points in the aforementioned time catamenia (March 1 to April 30, 2020). The coefficients for both A1/P1 and A2/P2 CP are non statistically pregnant.

Table two. Chief Market place Spreads and PDCF Usage

| (one) | (2) | (3) | (4) | (five) | (6) | |

|---|---|---|---|---|---|---|

| Pledged | -0.045 | -0.123 | 0.109 | 0.108 | -0.311*** | -0.274*** |

| (0.123) | (0.084) | (0.105) | (0.072) | (0.058) | (0.003) | |

| Sample | A1P1 CP | A1P1 CP | A2P2 CP | A2P2 CP | CD | CD |

| Obs. | 13,402 | 13,397 | 7,390 | 7,383 | 7,895 | seven,886 |

| R-squared | 0.428 | 0.696 | 0.583 | 0.799 | 0.158 | 0.311 |

| Day Atomic number 26 | ✔ | ✔ | ✔ | ✔ | ✔ | ✔ |

| Issuer Atomic number 26 | ✔ | ✔ | ✔ |

While these associations are suggestive, nosotros are able to dig farther into the data to attempt to get a better sense of the mechanism at work. Nosotros do then by comparing outcomes for securities that are "dealer-placed" versus "directly placed". Direct placement corresponds to most 20 pct of full issuance of CP and CDs, with the remainder being dealer-placed. Our hypothesis is that being able to pledge CP and CDs enhances the ability of the dealers to provide intermediation services for those securities. Such a mechanism would be consistent with the findings of Carlson and Macchiavelli (2020) regarding the furnishings of the emergency lending facilities for dealers from the 2008 financial crunch. If that enhanced ability is passed on to the issuers of the securities, then nosotros would expect that there should be increased issuance of dealer-placed CP and CDs that are pledged equally collateral but not for issuance of directly placed CP or CDs.

We carry this test by repeating the regressions above separately for dealer-placed and directly placed securities. The results, shown in Tables 3 and four, are in line with our hypothesis. As shown in Table 3, nosotros detect positive effects on issuance volumes for dealer-placed CP, but not on directly placed CP.9 This finding suggests that being able to use CP equally collateral at the PDCF enabled the dealers to support larger CP issuance volumes. The minor and negative coefficient for direct placed CDs in column (3) suggests that these CDs are less likely to be pledged on the issuance date. Equally shown in Table 4, we find that the dealer-placed CDs pledged to the PDCF had lower rates in the primary market than similar dealer-placed CDs that were non pledged to the PDCF. For loftier-quality (A1/P1) dealer-placed commercial paper the sign on the coefficient is again every bit expected, but it is not statistically significant. For directly placed commercial newspaper in that location is no issue. Thus, these results are consistent with the thought that the PDCF enhanced the ability of the dealers to provide intermediation services and that this do good was passed on to their customers.

Tabular array 3. Directly vs Dealer Placement and Chief Market Issuance

| (one) | (2) | (three) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|

| Pledged | -0.002 | -0.004 | -0.010*** | 0.307*** | 0.526*** | 0.065 |

| (0.009) | (0.004) | (0.002) | (0.108) | (0.188) | (0.096) | |

| Placement | Straight | Straight | Direct | Dealer | Dealer | Dealer |

| Sample | A1P1 CP | A2P2 CP | CD | A1P1 CP | A2P2 CP | CD |

| Obs. | 319,738 | 92,540 | 639,324 | 319,738 | 92,540 | 639,324 |

| R-squared | 0.329 | 0.209 | 0.007 | 0.238 | 0.263 | 0.02 |

| Day Atomic number 26 | ✔ | ✔ | ✔ | ✔ | ✔ | ✔ |

| Issuer Fe | ✔ | ✔ | ✔ | ✔ | ✔ | ✔ |

Table 4. Direct vs Dealer Placement and Primary Market Spreads

| (ane) | (2) | (3) | (4) | (five) | (6) | |

|---|---|---|---|---|---|---|

| Pledged | 0.39 | - | - | -0.131 | 0.091 | -0.272*** |

| (0.249) | (0.087) | (0.07) | (0.003) | |||

| Placement | Direct | Straight | Direct | Dealer | Dealer | Dealer |

| Sample | A1P1 CP | A2P2 CP | CD | A1P1 CP | A2P2 CP | CD |

| Obs. | one,395 | 310 | 499 | 12,429 | 7,145 | seven,431 |

| R-squared | 0.692 | 0.745 | 0.636 | 0.703 | 0.809 | 0.285 |

| Solar day FE | ✔ | ✔ | ✔ | ✔ | ✔ | ✔ |

| Issuer Atomic number 26 | ✔ | ✔ | ✔ | ✔ | ✔ | ✔ |

References.

Carlson, Mark, and Marco Macchiavelli (2020). "Emergency Loans and Collateral Upgrades: How Banker-Dealers Used Federal Reserve Credit During the 2008 Fiscal Crisis," Journal of Financial Economics, vol. 137, no. 3 pp. 701-722.

Li, Lei and Li, Yi and Macchiavelli, Marco and Zhou, Xing (Alex) (2020). "Liquidity Restrictions, Runs, and Central Bank Interventions: Prove from Money Market Funds," (December 29, 2020). Available at SSRN: https://ssrn.com/abstract=3607593.

Please cite this annotation every bit:

Carlson, Mark, and Marco Macchiavelli (2021). "Primary markets for short-term debt and the stabilizing effects of the PDCF," FEDS Notes. Washington: Board of Governors of the Federal Reserve Arrangement, June 18, 2021, https://doi.org/10.17016/2380-7172.2917.

Disclaimer: FEDS Notes are manufactures in which Board staff offer their own views and present analysis on a range of topics in economics and finance. These articles are shorter and less technically oriented than FEDS Working Papers and IFDP papers.

Source: https://www.federalreserve.gov/econres/notes/feds-notes/primary-markets-for-short-term-debt-and-the-stabilizing-effects-of-the-pdcf-20210621.htm

0 Response to "what evidence is necessary to demonstrate the ability to defer settlement of short-term debt"

Post a Comment